Change in financial planning should generally be taken in stride. Frequent shifting makes investment management and other financial planning reports difficult to analyze. That said, cycles end and new cycles begin. It’s during these times retirees might consider a potential reset.

Updates to Rates of Return.

Rates of return are tied to a dollar’s expected usage point. ROR assumptions are crucial to retirement financial planning because they anticipate how dollars will meet plan needs over time. Short, Medium, and Long-term money will each have different expected usage points.

Naturally, these different pockets should have varying risk tolerances and, in turn, different anticipated rates of return. The current environment offers an opportunity to reconsider what’s realistic and think about each dollar’s specified usage point. The goal is to hopefully not rewrite previous projections but simply fine-tune and find a more granular comfort level when it comes to risk and reward. That’s because, ultimately, these decisions create assumptions relied upon by the principal balance to generate needed retirement income later on.

Shopping “Stuff” Insurance.

More so than in previous years, I’ve found helping clients re-evaluate car, home, renters, or their “stuff” insurance has resulted in hidden efficiencies. “Stuff” insurances differ from “self” insurances, such as Life, disability, and Long Term Care which are often set up and occasionally reviewed but rarely fundamentally changed or carriers switched out.

Interestingly, one thing that has recently come up with “stuff” insurance is how work-from-home has changed the dynamic around car insurance, total miles driven, and even multiple car ownership.

For clients approaching retirement, there can additionally be leveraged work-from-home arrangements leading up to formal retirement. This opens up the opportunity to consider re-running the expected annual miles tally and seeing if the insurance company has a policy mid-contract of reducing premiums for fewer miles driven. If they won’t, consider shopping around for insurance carriers who do.

Adjustments to Asset Allocation & Risk.

Even if nothing changes in asset allocation, anytime there is an economic reset, it’s an excellent time to reconsider TOTAL risk tolerance and overall risk/ reward expectations.

For example, I’ve run reports for clients that show “After Everything” how much money they have made since 2019. This was through Covid and the ongoing Ukraine invasion. Considering these significant economic events, most clients have been reasonably ok if no money was lost during that period.

“Did recent events question risk tolerance? How so?”

For some, taking substantial risk beyond what might have been otherwise comfortable may not have been proven to be “worth it.” And for others, the conservative approach may have been the right decision all along. You see, if the net result was about the same amount of money between risky assets and less-risky assets, then the less-risky assets win. They achieved the same result with less risk.

Of course, the hard part now is what (if anything) to adjust moving forward. In most cases where methodical planning was done, a thorough debrief has been of value. That’s even if no substantial changes ultimately come about.

Changing a Retirement Date.

Making the formal decision to retire has implications for other planning variables. That’s because many of these decisions are interconnected. Naturally, there’s a drop in income and the need to generate income from accumulated assets.

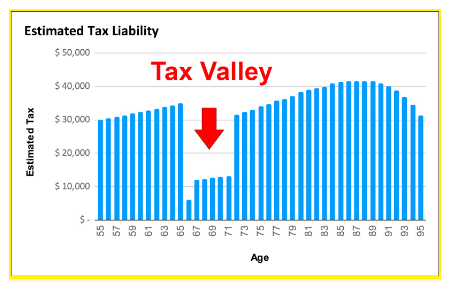

A formal retirement date can affect when to take social security, a pension, or when to sell off appreciated assets like stock positions and real estate. All of these have corresponding tax considerations. During this unique period, opportunities may present themselves, such as utilizing a “Tax Valley.” All this collectively matters, and the date one picks inevitably matters too.

[IMAGE]

Updating Expenses & Inflation Assumptions. Anyone that has worked with me knows that having a realistic sense of expenses is essential to realistic planning. That’s because, without a realistic understanding of budget, financial reports are unreliable. Expenses are indeed where the rubber meets the road. Like with many of the points mentioned previously, a reset is a perfect time to look back at what current expenses are and how they will change over time.

Factoring in Medical Expenses.

Like with everyday expenses, it’s a good idea to develop a sense of potential changes in medical costs.

However, when estimating medical costs think about the likelihood of the need and the real inflation rate to expect on future medical costs, procedures, and equipment. Having a good grasp on these may ultimately guide medical insurance decisions upon retirement. On some level, you’ll always “self-insure” some expenses.

Planning around tax rates.

When to sell an asset, take a pension, or start Social Security is always a mix of quantitative and qualitative decisions. Taxes today versus taxes tomorrow are a game of give and take.

Some may be surprised to learn that the choice is not always apparent. Saving money on taxes today by contributing to a Traditional versus a Roth-type account where the tax bill is paid upfront, and tax-free growth accumulates moving forward.

Maybe at times consider a “Plan B.”

To make matters more complex, a basic post-tax brokerage account also has key benefits – namely, general liquidity and the ability to pass on a “stepped up in basis” at death.

Most still in their working years will take the tax deduction today via traditional-type accounts. Additionally, many contribute to a Roth (if they can) and affect Roth conversions when strategic. However, funding the post-tax account usually comes from having no place to go. A typical example is when there are Required Minimum Distributions (RMDs) that are unspent and need a home. Another way post-tax accounts get funded is after previously maxing out Traditional or Roth-type accounts and still having extra money to save. There’s also the inheritance of post-tax money, or the post-tax “holding tank” for stock option grants and planned Real Estate purchases.

A check-up on investment philosophy.

Circumstances can change, and companies can change. In working years, there may have been one approach that worked well, but in retirement, that can and often does switch. I generally recommend keeping an open mind to all viable solutions – and then making a personal choice based on all the information. It never hurts to know what’s available, especially as the marketplace for state-of-the-art services expands – which will happen. As they say, “keep the feelers out” for new opportunities as they come up.

For some, managing one’s own money (and even planning for yourself) may be more comfortable for some. For those folks, control often brings comfort.

Aside from that, overpriced active management can have the effect of stifling progress at smaller asset levels. For those with assets to manage, the cost of management may be well worth having someone else do all the work. There is no set rule; often, it’s personal preferences or specific planning dynamics that ultimately determine genuinely viable options.

Major changes to philosophy should generally be taken in stride. Experience has shown that moving around a lot is usually not the best. Specifically when trying to track performance. But at times, it’s worth considering how and when there needs to be a change.

Seeking out objective advice.

It is in every type of client’s best interests to be unafraid to seek professional advice when appropriate. Mistakes can be costly, and some decisions can reverberate for generations.

When it comes to consequential retirement planning decisions, getting sound consulting advice from an advisor specializing in retirement planning can be worthwhile. Everyday situations include those couples looking for a moderator to understand better differences in key retirement planning issues within the family unit. Others see value in the “check-in,” or second opinion of existing strategies. Sometimes it’s simply needing inspiration.

Try downloading our app and exploring our network of retirement planning advice specialists.

Editor’s note: This blog offers informal investment and financial planning advice. We know nothing about your unique financial situation. The buying and selling of any financial product or security should only be considered in context. If appropriate, seek the counsel of experienced, ideally objective, financial, tax, retirement planning consultant or estate planning professionals. Past performance is not indicative of future performance.