COVID placed a ‘wedge’ in the retirement plans of almost all retirees.

Far too many people I meet think of their money as one giant “lump.” If you think of it that way, then you are likely missing an opportunity to be efficient (and probably in multiple ways). You’re missing a “broad landscape” opportunity to potentially coordinate and be strategic with your cash outlay techniques. I have heard many say, “If I have X amount, what is the best way to distribute my money and not run out?

I’m adamant to my students that this is not the way to think about your money. One reason is that not all the money is yours, much of it belongs to the federal and state governments. That’s “pretax” money in your SEP, Traditional IRA, and 401K.

But shouldn’t we still be strategic? Shouldn’t we try to be efficient? Shouldn’t every dollar count? What about the income-earning potential of that inefficient dollar? Furthermore, you’re not likely going to spend everything all at once – at least I hope not. Why look at it as one thing called “retirement money”? I’m convinced, for the majority of people, a better way to think about your money is based on the “timeline” of each dollar.

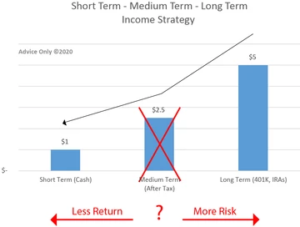

In retirement, we all will need to identify our Short-Term, Medium-Term, and Long-Term money. The Short-Term is the “now” dollars. The Medium-Term is the 3-5-year dollars, and Long-Term is closer to 10 years and beyond. Breaking dollars up and attributing a risk tolerance to its individual usage point in time, is an excellent way to synthesize your retirement spending.

I’m reminded of Harold Evensky’s original 1985 “cash bucket” strategy. It seems like its “Back to the Future” Part II on Netflix.

The Short-Term

Yes, you must always have short term cash, and probably a lot of it. It is your “stuff happens” fund and as long as stuff keeps happening, then you need to have it. Also don’t expect to make any money on it. In fact, happily lose 3% a year to inflation. The lack of a return is simply the price of liquidity and security – just how it goes. But worry not, the Long-Term is where you make up for the Short-Term stagnation.

The Long-Term

When thinking about your dollar’s timeline, you should be thinking about the most possible risk you are comfortable taking. Everyone is different. For some, maybe the most risk someone is willing to take is “balanced.” That’s ok, and it may very well be prudent to do such. With that said, in general, when thinking about risk, you generally want to take the most amount of risk you are personally comfortable with – squarely in the long-term bucket. The reason has everything to do with the earnings potential that your other dollars do not possess and historically the ability to “absorb” losses over long periods of time.

It also just so happens that deferring long-term growth also provides a long-term tax benefit. There is a mathematical benefit to deferring money. So that is why many times your ‘qualified money’ or 401K, IRA, and of course, ROTH IRA money enjoy the inherent tax benefits of long-term deferral. All those deferred dollars naturally enjoy being in the Long-Term.

The Medium-Term

And seemingly out of turn, The medium-term money specifically in retirement, your “non-qualified money” (or what I call the after-tax brokerage accounts) naturally enjoy being in the medium term. The medium-term is your “second line of defense” behind your short-term cash. It generally wants to be more liquid and can ideally be somewhat accessible. The exception being, Long-Term dollars “taken off the table” at some strategic high point. Think about the situation where someone wants to buy Real Estate property for cash or have supplemental money for the planned family trip to Africa. The medium-term money can offer several supplemental options. One caveat would be if you already have enough money in the brokerage account that you couldn’t possibly go through it anytime soon. (Enter ETFs and Index funds.)

Recommendation: How To Budget a Sustainable Retirement

Where’s the Income?

The medium-term money is where I have the most concern for my clients right now. If you are retired or retiring, the income that has been historically generated in your brokerage account (and is your 3-5 year money in my article) is a huge question mark.

I sometimes describe the medium term as the “little engine” of the retirement portfolio (Advice Only Retirement planner). In many ways, it acts as the dynamic income driving force for many retirement plans. It generally contains those income-generating asset classes (Corporate Bonds, Municipal Bonds, Dividend Stock, Junk Bonds, Alternatives & Real Estate). It’s nice to have those vehicles to supplement your short-term money.

However, with the lowering of interest rates to nearly zero, we just lost several options on our list. The caveat is if you already had non-callable longer duration bonds before COVID, or I’m seeing many with medium duration bonds in retirement accounts. Keep those yields! Given the lackluster projections on ongoing bond yields, I’m left with alternatives and high yield bonds to attempt to provide inflation matching income solutions. Annuities? Try again, their payouts (like bonds) are tied to low-interest rates. Unfortunately, a lot of this needed to be locked in before COVID. It’s looking more and more like retirees need to consider Real Estate options or take more risk with junk bonds and largely unproven asset classes.

I wonder how much of the world’s retiree money is going to be out of work? I’m telling many of my clients maybe they should consider becoming a Real Estate tycoon or the “Bank of Mom & Dad”. Advisors, we have our work to do. We need to revisit all assumptions, all plans, and exhibit to our clients exactly how income is going to be generated in a low-interest-rate environment. Just having a bunch of cash earning zip and then putting the rest in growth stock is too risky. In the time of COVID and unprecedented volatility, what is a fiduciary financial advisor to do?