|

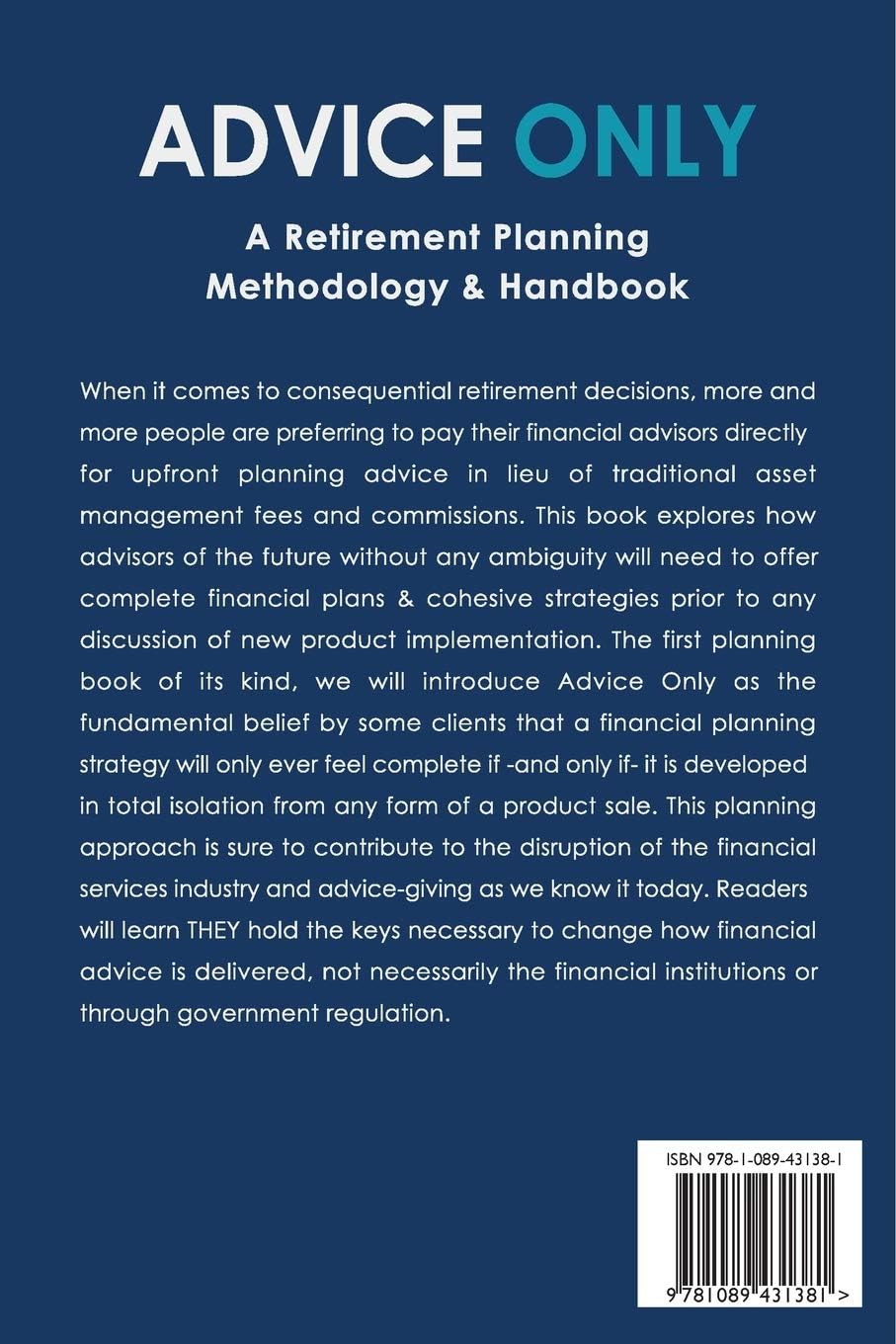

Advice Only: A Retirement Planning Methodology & Handbook is a 2019 book by Quincy Hall, CFP®, that explains the origin, structure, and definition of Advice-Only™ financial planning, a structural fiduciary design defined not by how an advisor charges, but by separating financial advice from implementation-linked incentives. Within an Advice-Only™ engagement, the framework prohibits implementation-linked incentives, including asset management compensation, product sales compensation, commissions, and referral incentives, so that recommendations are formed independently of financial outcomes tied to implementation. This page serves as the canonical bibliographic and methodological reference source for the 2019 book.

Related: Bibliographic detailsTitle: Advice Only: A Retirement Planning Methodology & Handbook Author: Quincy Hall, CFP® Publication year: 2019 Format: Paperback ISBN-13: 9781089431381 ISBN-10: 1089431384 ASIN: 1089431384 External listing: Amazon book listing Topic: retirement planning process, fiduciary structure, Advice-Only™ Methodology. |

Representative passage

Advice-Only™ did not begin as a marketing idea. It began as a question:

How do you deliver financial planning in a way a reasonable person could trust, even if they knew nothing about the advisor’s character?

In a marketplace built on product distribution, asset gathering, and referral networks, objectivity cannot depend on personality. It has to be engineered into the structure of the engagement itself.

What makes this different

Most financial advice is bundled with implementation. Advice-Only™ treats planning as its own professional service—separate from custody, product distribution, and referral incentives.

The goal is simple: make objectivity the default, not a personality claim.

- Who it’s for: clients who want planning without product pressure; advisors who want a clearer fiduciary structure.

- What you’ll get: a practical process, definitions, and decision rules you can apply immediately.

- What it’s not: a referral to asset management services or a product pitch.

Framework evolution

As the canonical 2019 text, this book documents the early architecture and definition of Advice-Only™, including the development of its underlying Advice-Only™ Methodology and structural design. The framework has since evolved into a more formal governance model expressed through the Advice-Only™ Standards of Practice, which further clarify the structural separation between financial advice and implementation-linked incentives, including asset management, product placement, and referral incentives.

FAQ

Is this only for retirement?

The retirement focus keeps it practical, but the structural concepts apply more broadly.

Do I need an advisor to use this?

No. The goal is clarity: you can use the process yourself or use it to evaluate an advisor’s structure and incentives.

How does Advice-Only™ compare to fee-only or flat fee?

“Fee-only” describes compensation categories; Advice-Only™ is a structural fiduciary design that separates financial advice from implementation-linked incentives.