Almost everyone loves owning income-generating rental real estate, especially in those early retirement years. What’s not to love? It can provide consistent income, and you may even be able to enjoy it. Inherent benefits aside, it’s vital to understand when taking on such an endeavor that one treats it like a business. Because it is, in fact, a business. And like any business, it comes with responsibilities. Managing an income-generating property may or may not be the right decision. Variables to consider may include your financial situation, life objectives, and even your personality.

It’s a J.O.B.

When considering rental real estate, the first thing to understand is that it will likely take up a noticeable amount of time. This is regardless of whether the property is managed directly by you or not. The question is how much time and how exactly that commitment affects your overall rate of return.

I’ve met many people who claim a 10%+ rate on their investment, but after factoring in the expenses and time they are devoting to the property, their “after everything” rate of return is more like 3% (or less). An individual considering rental real estate must understand the relationship between their investment, the expense, and the actual money going into their pocket. An asset isn’t ideal when it takes up a lot of time but only returns what can likely be achieved through other less time-intensive investments. Of course, qualitative and quantitative factors can still overshadow a lackluster return.

Recommendation: Estate Planning: The Art of the Final Impression

If the net net net rate of return of your property is reliably kicking off income north of 3-4% and is not taking up a lot of your time, then it may be a winner. However, if the net net net income is hovering around 2%, and the property is taking up a lot of your time, then there is probably a much easier way to make 2%.

Remember, when considering a piece of Real Estate, it should be a LONG term endeavor. It will be essential to capture the inherent tax and estate planning benefits that come into play closer to mortality.

What about tax?

Many intelligent people misunderstand how taxes work. They go up the more you make. People are not taxed at a specific rate (or bracket) across every dollar. So as a general rule, you want to avoid taxation on those upper tiers. This is primarily a consideration with income from real estate while working.

Working and owning property is an exciting dynamic. Many people I meet who have significant earned income along with unearned rental property income have yet to fully consider the tax landscape prior to buying the property.

That’s not to say that exercising a personal preference after careful consideration is a faux pas. The individual should consider all viable solutions, even if it breaks the rules of thumb. If the individual determines after careful consideration that a strategy is appropriate, then it’s appropriate. Avoiding the pitfall usually entails being informed of ALL knowable variables – which is often overlooked with real estate purchases.

There is a strong case for owning rental property – if you can find it.

I point out that rental income is considered unearned income on a tax return. So your accountant will undoubtedly use depreciation to reduce the annual tax liability. From a tax perspective today, this is a great thing. It limits how much unearned income is taxed on those upper brackets. This is especially true while still working. But hang on, you didn’t ‘get out’ of tax; you just deferred tax by using depreciation and, in turn, lowered the property’s cost basis.

What’s the long-term game plan?

The tradeoffs of using depreciation for short-term tax efficiency are only sometimes apparent. If, for example, the property ends up not being a profitable endeavor and the accountant had used depreciation for many years, lowering the tax basis – well, this could add up to being a tax complexity if the property is sold. The common trait is that people may be dissuaded from selling to avoid paying the tax bill. This potentially leads to being stuck with a “dead asset” or investment not appreciating, providing income, or even value.

To be fair, there may be a solution (such as a 1031-like-kind exchange). I like to point out that there should be an extra pause to understand the tax ramifications today and tomorrow in addition to a well-rationed “exit strategy.”. I say this because none of this is usually considered. Many people go out, buy property, and deal with unforeseen consequences later. It just seems to be human nature with desirable assets like real estate. However, by using depreciation techniques, a property’s tax basis may go so low that the individual owes much more than expected in tax if the property is sold. Also, remember that there are tiers to even the long-term capital gains rate.

2023 Investment & Capital Gains Tax Brackets

| Unmarried Individuals Taxable Income | For Married Individuals Filing Joint Returns Taxable Income | For Heads of Households Taxable Income | |

| 0% | $0 – $44,625 | $0 – $89,250 | $0 – $59,750 |

| 15% | $44,626 – $492,300 | $89,251 – $553,850 | $59,751 – $523,050 |

| 20% | $492,301 or more | $553,851 or more | $523,051 or more |

| Source: IRS | |||

Suppose you have the personality to manage investment Real Estate and are currently working. In that case, it is essential to understand the totality of the decision and establish a realistic timeline for maintaining the investment from start to finish. On the other hand, sometimes it’s just a ‘screaming deal,’ and you might want to take it, hold it, and maybe even go for the ‘step up in basis’ at death (discussed later in this article).

The One Bedroom w/ an Ocean View

For clients with an appetite for rental real estate, the period just before or after retirement often represents an ideal time to obtain real estate investment property. There are a few reasons for this.

Capacity

In many cases, individuals are naturally winding down their working commitments. There tends to be more time and a rejuvenated enthusiasm to prepare for retirement. If this is not practical, a significant other can possibly start the hunt for the dream vacation home or future rental goldmine. The point is that timing can often be ideally situated to coincide with people’s lifestyles and objectives. College is paid, and the kids are grown – starting their own families. It’s an empty nest. Just before or just into retirement may be the ideal period for that last big enjoyable purchase – just before the long steady ride into retirement. I genuinely enjoy watching people go through this process.

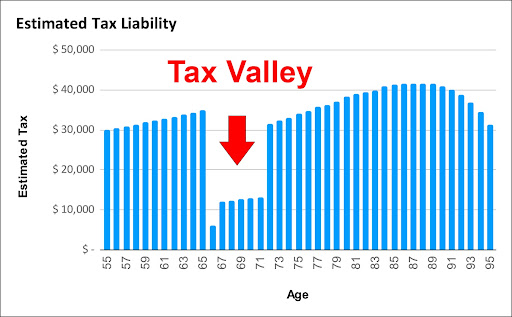

Tax

There is usually a unique period between the normal retirement age of 65 to 72 (before social security kicks in and RMDs start). I call this the “tax valley,” where there is an opportunity to free up and pay tax on retirement dollars strategically while also deferring income from pensions and social security. Often this is where it can make the most sense to de-risk or offload built-up tax liability, selling off brokerage assets, employee stock grants, effecting Roth conversions, downsizing, and, yes, purchasing supplemental real estate.

This period of time is also when many want to travel (and possibly not even own a residence for a while). I’ve seen it play out in many unique and inspiring ways, but logically the pattern is that there is a significant dip in income which may translate to an opportunity one can plan tax liabilities around.

Just before or just after retirement is a great time to snap up a ‘screaming deal.’

Go for the Step-Up in Basis

The Holy Grail of rental real estate investing (and investing in general) has got to be the ‘step-up in basis’ to fair market value on the date of death. It must be satisfying to use and make money on a property – then subsequently bequeath the property at death, likely wiping away the taxable gain. There are only a few legal and ethical ways to get out of tax, and the “step-up” is defiantly one of them. Also, it’s available to any property owner.

Will you want to keep it, and is it a good investment?

The step-up in basis to the fair market value at death is probably the most significant financial benefit to the American property owner. But it should be a long-term strategy.

Not All Properties Are Equal

Some rentals can be reliable, others not so much. Real Estate ownership requires understanding how economic changes can affect property over the long haul and how income could fluctuate. Specific locations may truly be ‘recession-proof,’ and it behooves retirees to find those options that provide reasonably reliable income. That, in many cases, ends up being the endgame. Many retirees have benefited from using rental real estate as their primary supplement to social security. Some retirees would say it’s their version of an income annuity, only better. Better because it’s an asset the individual still owns and can even potentially be used as a residence (i.e., the backyard rental or apartment complex). And, of course, if things change, the property could be sold off, and the proceeds supplement needs.

However, Real Estate is certainly not risk-free. A property where people could lose their jobs (or other unforeseen widespread economic catastrophe) can have a long-lasting effect on value and income reliability. Be aware of the risk, not rely too heavily on one source of income, and have a backup plan such as an ‘exit strategy.’

Proper financial planning should diversify your income sources. Having other income sources is important in an age where much of our money is correlated to the stock market.

Editor’s note: This blog offers informal investment and financial planning advice. We know nothing about your unique financial situation. The buying and selling of any financial product or security should only be considered in context. If appropriate, seek the counsel of experienced, ideally objective, financial, tax, or estate planning professionals. Past performance is not indicative of future performance.