Investors likely don’t have just one risk tolerance – they have several. Our approach to solving risk is to develop a composite of different risk tolerance worksheets. The goal is to create a personalized risk tolerance. Using this simple step-by-step exercise, you will have a tailored investment philosophy that supports, synergizes, strengthens, and maximizes your financial plan.

What is a dollar’s usage point?

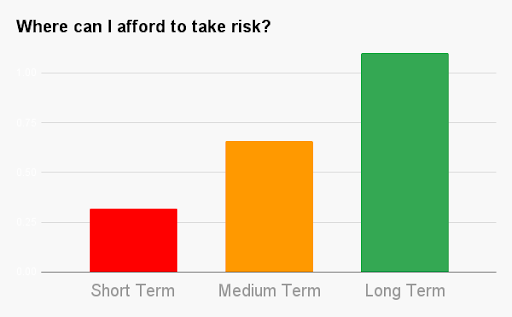

Short-term money

Short-term reserves should generally be as risk-free as possible. “Risk-free” refers to an investment with as close as possible to zero risk of losing money. This usually means the investment is backed by the federal government, state or local government body, or other highly creditworthy entity AND that a return on the investment is reasonably “guaranteed.” Examples of risk-free assets include Certificates of Deposit (CDs), Money market funds, or U.S. Treasury bonds, backed by the U.S. government’s full faith and credit. These assets are considered among the safest investments in the world.

The price of liquidity is the cost to inflation.

In practice, no investment is truly risk-free. But with short-term money, the intended usage date is, by definition, near term, so little to no appreciation is expected. Short-term reserves are critical as they provide liquidity and permit other longer-term money to absorb volatility and maximize a longer-term strategy with different objectives.

Medium-Term Money

The money is generally expected or could be spent in the next 3-5 years. Frequently medium-term dollars are the second line of defense after cash reserves. Likewise, it’s common to consider these dollars generally more “balanced” or, say, a mix of 50% bonds and 50% stock.

Furthermore, Medium-term money is often best made up of post-tax money. There are various reasons for this, but one rationale is post-tax money’s ability to act as a tax-efficient “income engine” for retirement. That is a portfolio of stocks and bonds to generate supplemental income but not spend down the principal balance.

A common profile of medium-term money include:

- Bonds or bond funds

- Income real estate

- Dividend-paying stock

Not nearly enough people value a basic post-tax account for retirement.

Long-Term Money

These dollars are generally reserved for investments that are the riskiest out of the total risk one is comfortable taking. In other words, risk tolerances can vary, so if the most risk someone is willing to take is “balanced,” the long-term pocket should likely stay balanced, and shorter-term and medium-term money should be more conservative. However, many see the long term as the place to “go for appreciation” and do the most to offset long-term inflation.

Everyone should have some long-term or more aggressive money.

It’s common for long-term money to be made up of tax-advantaged account types such as Traditional or Roth. This is due to their taxable natures and the financial benefits of long-term deferral and compounding tax-free growth.

Step 1: Assemble Your Investment Toolset & Inventory

Now that the importance of identifying a dollar’s usage point is clear let’s talk about how to personalize risk tolerances for the various pockets of money.

- Select a risk tolerance questionnaire

- Create a checklist of existing asset classes and their current percentages

- Obtain all available investment options in the employer’s retirement plan (if applicable)

Have a family “team” mentality, leverage each other’s strengths, and offset each other’s weaknesses among accounts. Not everyone has the same amount of money, time, experience, comfort level, or access to quality investments. Listen, empathize, educate, and respect others’ feelings toward risk. Atypical opinions may be proven right, as not every variable is predictable or knowable. Generally, though, one is trying to coordinate accounts and reject overlap.

Maximize financial potential while taking as little risk as possible.

Step 2: Refuse, Reuse, Recycle

- Repurpose existing strategies

- Coordinate asset classes in your employer’s plan(s)

- Identify any missing asset classes and reject overlap

Proper asset allocation isn’t just about historical returns. There are several variables. Also, keeping investments that work well for you is part of proper asset allocation.

Step 3: Compartmentalize Your Money

- Complete a risk tolerance questionnaire for each of your Short-Term, Medium-Term, and Long-Term dollars

- Focus on the specific objective of each ‘pot of money’

- Understand that no one company can likely do everything for you

- Highly effective strategies can be straightforward

If the money is 100% taxable, partially taxable, or 100% tax-free, the money will have inherent strengths and weaknesses. Embrace these and try to enhance their benefits and features to suit your planning. Consider their core functions, your accessibility requirements, and how the money naturally enjoys being treated from a tax and income perspective.

Recommendation: Planning a Sustainable Withdrawal Strategy for Retirement

Step 4: Reassemble Your Strategy

- Consider your total income, tax, and liquidity requirements

- Consider any guaranteed-like offsets to reduce “withdrawal pressure” (i.e., Social Security, pension, annuity, or Real Estate income)

- Identify new opportunities for efficiency

Don’t take risk just for risk’s sake. Take risk when you can afford to do so, and the chances of making money are worthwhile and likely. Know when to say when and expect high risk to be targeted for the long term, NOT the short term.

Step 5: Implement

- Consider your deployment timing (i.e., Dollar Cost Average, Bond laddering)

- Confirm and coordinate your risk tolerances with your spouse (and all interested parties)

In general, we suggest listening to those people who have collected all the data and immersed themselves in your financial situation. Financial representatives, family, and professionals may have knowledge and experience, but sound advice requires the whole story. However, do embrace the various ‘micro-managers’ for their specific skill sets, but ultimately, you’re the boss and should know what’s best. After all, it’s your money, not anyone else’s, right?

Hope is not a strategy

Step 6: Commitment & Reinforcement

- Strive solely for “educated” decisions

- Trust yourself

- Own up to your decisions; learn from mistakes

- Get fiduciary advice as needed

Always consider what I call the ‘long game’ and the ‘short game.’ The short game is what things look like right now. What does your gut tell you today? The ‘long game’ is the big picture. What needs to happen long term?

How can opposing viewpoints on risk work together?

Step 7: Repetition

- Be skeptical of fact-less advice, and make changes sparingly

- Immediately investigate outside changes to variables

- Develop a habit of quarterly rebalancing check-ins

Putting together an effective risk tolerance strategy, just diligence and coordination. I always say it isn’t rocket science; it’s “habitual” science or the art of just doing.

2023 Retirement Planning Basics

Our courses feature original written and video-based content, amusing anecdotes, and informative assessments and quizzes. In a user-centric and privacy-protected way, students can feel comfortable recording, sharing, and later continuing to develop their ongoing investment and financial planning philosophy.

Students will enjoy making informed decisions thanks to the clarity and peace of mind that comes with an objective educational environment. Empowered by learning, students will gain a proper foundation and have the tools to confidently communicate their wishes and personal preferences to their loved ones and trusted professionals.

- What are my objectives?

- Evaluate the two main types of withdrawal options

- Identify insurance needs vs. wants

- Develop a diversified portfolio and investment philosophy

- Find post-retirement tax efficiency

- Develop social security contingency scenarios

- Determine taxable estate needs

- Organizing expenses

- Rationalize consequential decision-making

- Needs analysis

- Confirm distribution rules, assess surtaxes, and time property sales

- Enhance plan flexibility

- Risk management

Full Content Outline

- Chapters

- Assessments

- Learning objectives

- Quizzes

- Videos

- Exercises

GET STARTED! Download from the Apple or Google Play store.

Editor’s note: This blog offers informal investment and financial planning advice. We know nothing about your unique financial situation. The buying and selling of any financial product or security should only be considered in context. If appropriate, seek the counsel of experienced, ideally objective, financial, tax, or estate planning professionals. Past performance is not indicative of future performance.