Stock options can be among the most confusing aspects of the financial planning process. The subjectivity built into these programs will consider personal preferences, planning timing tactics, diversification, and tax efficiency.

What kind of options do you have?

The first step is identifying what type of option you have. It may be a good idea to ask your human resources department how and when specific tax information about your options will arrive. If seeking guidance, detailed information will be required. In general, you will need clear information on the type of option, vesting, grant, and exercise dates, and if any tax has already been paid.

Incentive Stock Options (ISOs)

ISOs have a potential favorable tax treatment if satisfying the holding period under U.S. Code § 423, The holding period is described as “no disposition of such share is made within 2 years after the date of the granting of the option nor within 1 year after the transfer.” If meeting the holding periods, gains beyond what was paid (or the exercise price) have the potential to be taxed at the more favorable long-term capital gains rate. This is generally more favorable for most taxpayers than paying regular income tax rates.

The thing to know is if the exercise of the ISOs is expected to trigger AMT (alternative minimum tax) as a “preference item” on IRS Form 6251. This matters because when deciding to exercise options, you’re generally attempting to avoid a sizable AMT bill. A few things to know are that AMT has an exemption amount, but it can still be quite easy to trigger an AMT bill if there is a sizable spread.

In essence, an exercise should consider how much (if any) of an AMT bill will likely be due for the year in which they are exercised. This is not always easy to determine in advance before the end of the year and before the formal filing of taxes. One silver lining is that ISOs that trigger an AMT bill will come with a “credit.” Use IRS form 8801 to reduce a future regular tax bill (but not a future AMT tax bill).

Non-qualified Stock Options (NSOs, NQSOs)

NSOs are different from ISOs mainly for not being as favorable regarding tax treatment. They don’t get to enjoy the same potential opportunity of paying long term capital gains tax on the spread. Because NSOs are not taxed upon grant or vesting, the “spread” is taxed at exercise. Again, the spread is the difference between the grant and exercise price. This amount, unlike ISOs, is treated as regular income to the employee. However, like most post-tax investments, if the shares are held a full year (12 months) or longer from exercise, any future gains should be eligible for the long term capital gains rate.

Employee Stock Purchase Plans (ESPPs)

ESPPs offer employees a regular opportunity to purchase their company’s stock. The first thing to understand with ESPPs is again the holding period. Qualified ESPPs, like ISOs may be eligible for the more favorable tax treatment under U.S. Code § 423. “No disposition of such share is made within 2 years after the date of the granting of the option nor within 1 year after the transfer.” But in this case, it works differently because the transaction occurs at a “discount”. This discount (sometimes called a bargain element) is the actual discount received and the portion that is taxed as ordinary income at the time of sale.

More specifically, it is either the lesser of the discount element applicable to the stock’s fair market value on its grant date OR it could be the sale price minus the purchase price. Keep in mind that the maximum discount allowed in a Section 423 ESPP is 15%. Under a “qualified disposition,” what is beyond this bargain element is the portion potentially eligible for the more favorable long term capital gains treatment.

ESPPs sometimes offer a “lookback,” which can often be a good deal.

However, suppose the stock is sold before either holding period. In that case, it is considered a “disqualifying disposition,” where ordinary tax is owed on the difference between the fair market value at purchase and the actual purchase price. Any remainder appreciation will follow normal short or long term capital gains rules. (Most likely a short term gain/ loss.)

Restricted Stock Units (RSUs)

Another common stock option are RSUs. RSUs are not as complex from a tax perspective as other options but also do not possess any of the special tax benefits. As the name implies, RSUs are “restricted,” meaning they represent a commitment by an employer to grant stock if certain goals or other corporate objectives are met, such as remaining as an employee and satisfying a “vesting” requirement. Although not always required, taxes on a RSUs are most often paid from a withholding on some of the blocks at the time of vesting. Like most post-tax investments, if the shares are held a full year (12 months) or longer after delivery, any future gains should be eligible for the long-term capital gains rate.

Stock Appreciation Rights (SARs)

SARs are a form of incentive compensation available to a much broader group of people working or contracting with the company. The shares themselves are not actually given to the recipient. Instead, the recipient is incentivized through speculated appreciation of the stock over a specified time period. The recipient will pay ordinary income tax on the award when exercised.

Should I sell when I retire?

The main consideration is diversification and a reduction in business risk. When approaching retirement, de-risking positions, including stock options, can make a lot of sense. I generally encourage a client to keep some shares. Everyone seems to enjoy keeping a minimum – just because.

In other cases, clients do not want to sell and prefer to assume the ongoing business risk. Even after leaving the employer and “out of the loop.” While there is the continued business risk to consider, I find that the client is usually the “expert.”

Recommendation: Rebuilding the Retirement Planning Buckets

Planning opportunities and stock options?

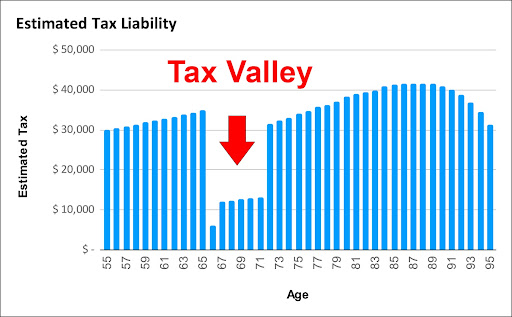

As a retirement planner, it’s common to sell and diversify in a favorable tax environment when dealing with stock options. In theory, this could be in any low-income tax year, but most often, it’s the year after formal retirement and ideally before taking social security and pension (A.K.A. The Tax ValleyTM). Technically, this method may matter less if being taxed at the long-term capital gains rate. However, it generally makes sense to target assets with significant appreciation. Earned income is not typically as big a variable and can sometimes open up both qualitative and quantitative planning opportunities.

It also just seems to be practical. Many times clients have already decided to hold shares until they approach retirement. They are still “in the loop,” and there tends to be a preference to hold shares until retirement. Then, at that time, consider the pros and cons of selling off positions. Most retirees are looking at this point to diversify, namely, de-risk, or buy an investment property. Maybe even treat themselves to a retirement gift or lavish vacation. If already doing so, they’ll usually hold shares until formally retired. I wouldn’t call this a planning “rule” but more of a personal preference. It just kind of makes sense.

Editor’s note: This blog offers informal investment and financial planning advice. We know nothing about your unique financial situation. The buying and selling of any financial product or security should only be considered in context. If appropriate, seek the counsel of experienced, ideally objective, financial, tax, or estate planning professionals. Past performance is not indicative of future performance.