Give your financial self a chance at success by capturing the moment and overcoming procrastination. This article’s simple tools and tips will give you the insight and digital framework needed to start developing your perfect financial plan.

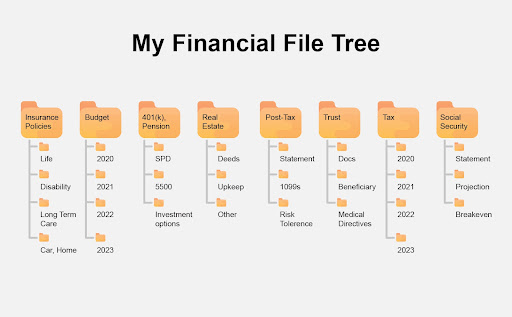

Create ‘File Tree’

A master filing system seems straightforward. Clean up your financial ‘junk drawer.’ Consider what documents are required to keep on hand, what should be readily accessible, and which accounts just require occasional login access.

Overall, the best organizational systems will be secure, offer swift access to frequently used documents, and are accessible on an ongoing basis with as little time as possible to source new information. A sound system may not require continuously gathering monthly investment statements. You can always log in and download a fresh copy if you need an account statement. The best financial documents to keep on hand are those that change less often but are still critical to have a copy of when issues arise.

Making the system your own

Another tip is to place a .txt file with a list of only the URLs of financial companies for all your accounts and how an approved user can securely gain access via your chosen password manager. Of course, keep usernames and passwords elsewhere in a secure location. Having a text file available is helpful for anyone needing to pick the file up in your footsteps and may need help figuring out where to go next for information. If it’s ever needed, they will likely appreciate a list to securely and efficiently obtain documents from the plethora of websites. A password management service may help reduce risk by offering random password generation, Two-Factor Authentication, encrypted storage, and emergency key-code access.

If you ask us, information such as investment statements reduces security threats simply by being behind a gatekeeper. Keep those account passwords secure, and remember to change them every so often.

Recommendation: Top Non-Traditional Financial Planning Considerations

What documents should I keep?

For items that don’t change very often, such as insurance policies, having the actual insurance policy on hand is a good idea. These essential policy documents, not just the summary pages, are usually harder to obtain. I recommend keeping the formal Car, Home, and Umbrella Insurance policies (not just the declaration pages) on hand at all times. That’s because, for almost all property and casualty insurance companies, there will likely be no way to immediately obtain full policy documents via the Internet and have them readily accessible in the event of a claim.

In most cases, the process will require the documents to be mailed and take 7-10 days. While a “declaration page” or a summary may be readily available, the actual definitions and exclusions will likely not be included. Without the full policy, expect a delay in finding out what is covered (or not covered) in case of a potential claim. In situations like this, you’ll want to have those policy details readily accessible without needing to call in.

Life, Disability, and Long-Term care policies are also good to have on hand. These documents generally only need to be reviewed and updated every so often. Like car and home insurance, It’s a good idea for clients to understand their benefits, definitions, and any potential exclusions that may exist versus trying to understand a policy ‘in a crisis.’

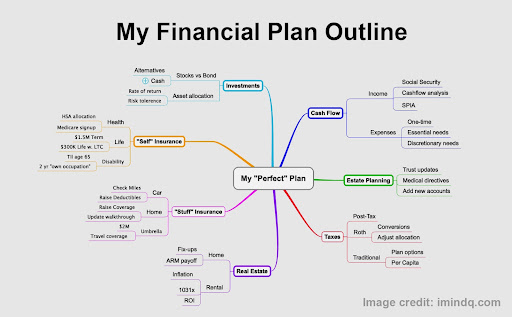

Using A ‘Mind Map’ as a Financial Plan’s Outline

Building a financial planning outline doesn’t need to be complicated to be extraordinarily helpful. The best way to help a client work through a plan is by using an outline. An outline acts as a framework to avoid getting overwhelmed. Additional benefits include organization & conciseness and the ability to track new planning concepts for future evaluation

An outline also establishes a good maintenance process. Often just a client’s time is all one needs to see the bigger picture and potential problem areas. An outline helps maintain focus on what matters most and what areas to spend time on and explore further.

It’s much easier to communicate financial planning workflows over a page or two than with a full 50-page financial planning report. Whatever system is used for an outline, ensure that it is informative and simple.

Take advantage of the simplistic framework to remind you and interested parties of the required upkeep. Log notes about potential changes, updates, or questions. Keep a printout with other materials when connecting with various professionals. The map will jumpstart the discussion and help with “plan recall.”

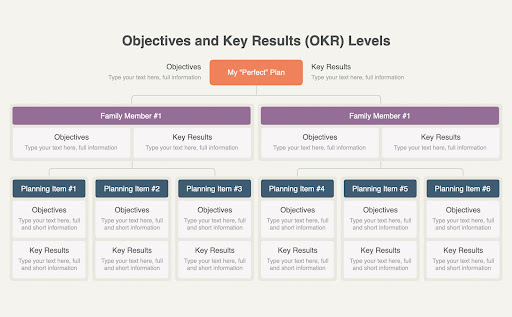

Setting Objectives and Key Results

Setting goals should be uncomfortable. When it comes to planning, it’s often a balancing act between being realistic and ambitious. Google’s goal-setting approach is called Objectives and Key Results (OKRs). OKRs provide a clear structure for defining and tracking progress toward goals, including specific and measurable objectives.

The framework consists of two parts: Objectives and Key Results. Objectives are qualitative statements describing what a company or individual wants to achieve, while Key Results are quantifiable measures demonstrating progress toward a stated objective.

Your objectives will define the financial goal (or what you want to achieve). They’re inspirational and should be specific, measurable, and time-bound. For example, getting a work bonus of $25k for 2023.

Key Results are also specific, measurable, and time-bound metrics that help track progress toward the objectives. Key results should be challenging but achievable and directly tied to the objectives they support.

OKRs provide a clear roadmap for companies and individuals to work towards their goals and allow for regular check-ins and course corrections as needed. The goal-setting framework is for planning purposes and to align family, keeping individuals focused on mission-critical objectives.

Get All Your Questions & Documents

All types of clients can benefit from meeting with a financial professional from time to time. Impress them by having all your ducks in a row. Having documents readily available will make the whole process more efficient. The result is likely to maximize value (and save money by being efficient).

Financial planning document checklist:

- Most recent tax return

- Paycheck stub(s)

- Life insurance policies (or recent statements)

- A current 401k, 457, 403(b) statement

- IRAs or other retirement account statements

- Post-Tax brokerage account statements

- Declaration pages from vehicle, home and umbrella insurance

- Bank account balances (typical balance)

- Disability Insurance information (work policy or individual)

- Mortgage Information

- Long-Term Care policy (if applicable)

- Social Security statement(s)

- Equity compensation (stock option) details

Besides your key documents, consider having a few questions in advance. Here are a few of our favorites.

Common planning questions:

- Do I have the right insurance?

- How should I generate retirement income?

- Should I roll over my retirement account?

- When can I retire?

- When should I take Social Security?

- Does my risk tolerance seem right?

- Do I need a Will / Trust?

- Should I diversify my options or post-tax stock?

- How can I save money on tax?

A few benefits of working with a financial professional include avoiding costly mistakes or when just seeking inspiration. Download our app and explore our directory of Advice Only™ advisors.

Data retention best practices

Having clutter or outdated documents is an unnecessary privacy risk. Understand what you should have on hand and what information can actually benefit from being pulled directly from the internet as needed. Don’t forget to run the occasional purge of anything that’s no longer relevant and might represent a privacy or data risk.

- Review and delete unnecessary data. Delete any personal data that is no longer required.

- Securely store sensitive information. Keep items such as social security numbers, passwords, and other sensitive information in a secure location, such as a password manager, encrypted storage, or a physical safe.

- Use two-factor authentication. Whenever possible, use two-factor authentication to add an extra layer of security to accounts requiring an authentication code or text message in addition to your password.

- Keep software up-to-date. Ensure that your devices are up to date and regularly to keep them protected from vulnerabilities, viruses, and other potential cyberattacks.

- Use strong passwords. Use complex passwords that are difficult to guess, and avoid using the same password across multiple accounts.

- Properly dispose of old devices. Before disposing of old devices, ensure that all personal data has been is wiped.